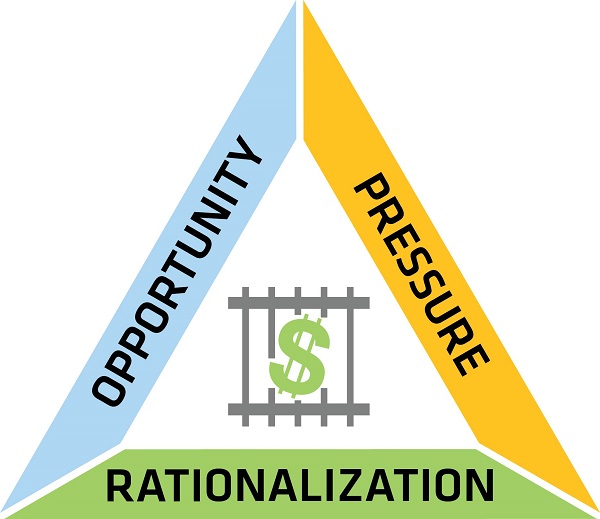

The college admissions scandal prompted multiple articles where the motivations of those involved illustrated the fraud elements of opportunity, pressure, and rationalization. When you know about the fraud triangle, you're more mindful of the risk of fraud so you can better carry out your oversight responsibilities.

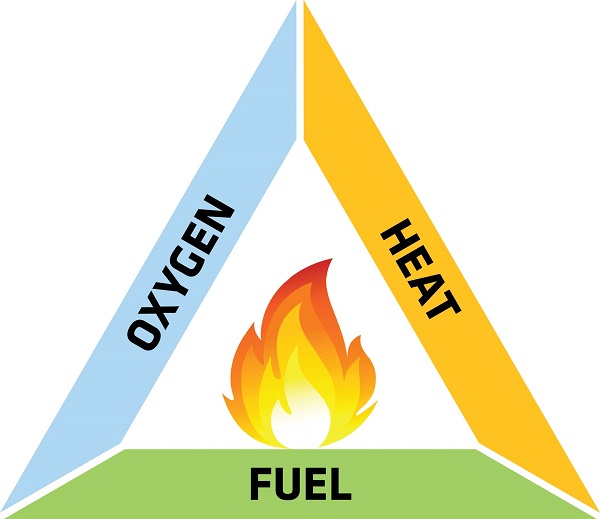

The Fire Triangle – Precursor to the Fraud Triangle

The Fire Triangle is a visual aid fire prevention educators use to illustrate the three elements a fire needs to ignite and burn: Oxygen, Heat, and Fuel. By removing just one of the three, you break the triangle and either prevent the fire or limit its damage by snuffing it out early.

The theory behind the Fraud Triangle is similar. Criminologist Donald Cressey first hypothesized the three primary factors leading to occupational fraud in 1951, and his work remains relevant today.

But while Cressey identified the fraud elements of opportunity, pressure, and rationalization, he did not use a triangle to illustrate their relationship.

The Fraud Triangle serendipitously emerged in the late seventies when a Brigham Young accounting professor, Steve Albrecht, conducted a fraud seminar at a large paper company. One of the participants recognized and pointed out to the professor the similarities between the various components needed for fire and fraud. Naturally, fire prevention is essential to paper company operations!

I realized that the Fire Triangle related well to fraud because firefighters know a fire can be extinguished by removing any one of the three elements.

I started calling the three elements that motivate fraud the "Fraud Triangle" … we can prevent fraud by extinguishing any one of the three elements.

Steve Albrecht, PhD, Brigham Young University

The triangle states that individuals are motivated to commit fraud when three elements come together: 1) some kind of perceived pressure, 2) some perceived opportunity, and 3) some way to rationalize the fraud as not being inconsistent with one's values.

Steve Albrecht, PhD, Brigham Young University

An opportunity, a control weakness, provides the oxygen for fraud.

Pressure provides the heat for fraud. And rationalization provides fuel for fraud!

As with fire, when you remove one side from the Fraud Triangle, you're better positioned to prevent fraud or limit its damage. Applying fundamental control techniques such as periodic review or verification and segregation of duties goes a long way toward reducing the element of opportunity.

Rationalization is fuel for fraud and can sound something like this:

- It's just a loan.

- No one will notice.

- I'll pay it back later.

- I'm underpaid anyway.

- I'm not hurting anyone.

- It's just a one-time thing.

- Everyone else is doing it.

- My employer can afford it.

Rationalization is the self-delusion required to mentally distance oneself from wrongdoing, separating the person from the act. Occupational fraudsters often act on impulse. Their decision-making process seldom weighs the probability of exposure and punishment to potential financial rewards.

Consider the schemes at Georgia Tech that involved four high-ranking officials.1 Did they consider possible bad outcomes? Perhaps one acted first, with the others succumbing to "everyone else is doing it." How did they rationalize their actions?